- Timeless Autonomy

- Posts

- "Professional" Status

**Disclaimer: All opinions and ideas expressed in this article are solely mine and none represent a recommendation or should be viewed as advisement of any kind to anyone to do anything.**

Top of Mind

The issue of “Professional Status” was a hot topic this week. Let’s break it down.

TL;DR: The most impactful change for most people is the elimination of the uncapped Direct PLUS loan that was available to both graduate and professional degree programs. It was a way to circumvent the caps on the Direct Unsubsidized loans if you could pass the credit check.

Here’s What Happened:

The Department of Education is proposing revisions to the definition of “professional degree” in federal regulations to align with the intent of Congress and to start to clarify eligibility for federal student aid programs that have changed through passage of HR 1 or “The One Big Beautiful Bill Act.”

Congress’s intent in Section 81001 of the bill is likely this: Limit overborrowing by graduate students and reducing the likelihood of federal loan defaults while still recognizing the higher cost of professional programs (medicine, law, dentistry, etc.). Of course, there’s the rub. Many feel important degrees are being left out of “professional” designation and therefore, lower available federal student loan caps.

Definition source: OBBBA explicitly tied the meaning of “professional student” to the existing regulatory definition of “professional degree” in § 668.2 in the Code of Federal Regulations, rather than inventing a new statutory (legal) definition.

Implication: The Department of Education was expected to clarify which programs qualify for the loan limits, but Congress itself did not alter the definition — it only applied loan limits based on that pre‑existing distinction.

Note: The distinction made in statute relate between what is a “professional degree” vs. a “graduate degree” is not new.

Here are the Federal Aid Programs and the OBBBA Changes:

Direct Subsidized (NOT available for graduate and professional degree programs)

Direct Unsubsidized: Prior to the OBBA , this was capped at $20,500 annually and $138,000 lifetime for both “professional” and “graduate” programs. In the OBBA, “professional” is being raised to $50,000 per year while the lifetime is being raised to a maximum of $200,000. In addition, “graduate” is being maintained at $20,500 per year while lifetime is being lowered to $100,000.

Direct PLUS (being phased out in 2026 as a result of the One Big Beautiful Bill Act). This loan had NO CAP and is the major negative change for both categories of degree programs. It filled in the gaps left by the caps in the Direct Unsubsidized loans for both annual and lifetime caps.

Direct Consolidation

Here’s a quick refresher on how laws are made and carried out and applicability to this issue:

Congress makes the laws, including HR 1. The Executive branch carries out the laws. The DOE is part of the Executive branch of government. (We in healthcare are more used to the work of the Center for Medicare and Medicaid Services (CMS) or the Food and Drug Administration (FDA)).

Each agency functions a little differently, but the process of rulemaking is similar. The agency develops and then publishes a proposed rule to update their interpretation of the law at either a regular cadence or to address a specific issue, such as in this case.

The current Secretary of the Department of Education is Linda E. McMahon.

This is a cabinet-level position. (Author’s Note: in the case of one-party control of the Presidency and both Houses of Congress, and particularly now when Congress is considered by many to be trying to carry out the agenda of this President—more easily done in a reconciliation bill where the Senate filibuster isn’t in effect—the way the agencies implement laws may be more closely aligned with the President’s agenda.)

Side Note and Potentially Relevant: The President Has an Executive Order Calling for the Closing of the Department of Education

The DOE’s loan portfolio is slightly under 1.6 trillion dollars. If the DOE closes, federal student loans would be transferred to another entity (likely Treasury or a designated financial authority). Borrowers would still owe their balances, repayment and collection would continue, but the administration of programs could change significantly.

This quote comes from a Fact Sheet about a March 2025 Executive Order:

The Executive Order directs the Secretary of Education to take all necessary steps to facilitate the closure of the Department of Education and return education authority to the States, while continuing to ensure the effective and uninterrupted delivery of services, programs, and benefits on which Americans rely.

So to summarize: The OBBBA, or HR 1, made changes to the federal loan program, and the new caps must be applied based on the classification of an educational program as defined by the federal government. In addition, the OBBBA eliminated the most generous program, one without caps at all, the Direct Plus program. To put this new law into effect and make it actionable for the public, the DOE will put out a proposed rule.

Here’s the current definition of a “professional degree” on the Code of Federal Regulation:

Professional degree: A degree that signifies both completion of the academic requirements for beginning practice in a given profession and a level of professional skill beyond that normally required for a bachelor’s degree. Professional licensure is also generally required. Examples of a professional degree include but are not limited to Pharmacy (Pharm.D.), Dentistry (D.D.S. or D.M.D.), Veterinary Medicine (D.V.M.), Chiropractic (D.C. or D.C.M.), Law (L.L.B. or J.D.), Medicine (M.D.), Optometry (O.D.), Osteopathic Medicine (D.O.), Podiatry (D.P.M., D.P., or Pod.D.), and Theology (M.Div., or M.H.L.).

The DOE has made a lot of progress in preparing for their public proposal. From “Inside Higher Ed,” a summary of the proposed change to the CFR:

Under ED’s [Department of Education] latest proposal, in order for a degree program to count as “professional” and gain access to the highest amount of federal loans it must:

Require a level of skill beyond that of a bachelor’s degree

Be a doctoral level degree (with the exception of a Master’s in Divinity)

Require at least six years of academic instruction (at least two of which are post-baccalaureate)

Involve a profession that requires licensure

Be included in the same four-digit CIP code as one of 11 professions explicitly mentioned in the regulation

What is a CIP Code?

The Classification of Instructional Programs (CIP) was developed by the U.S. Department of Education's National Center for Education Statistics (NCES) to map programs to a shared understanding of what a given program of study includes, collect data from schools on programs of study offered, and create reports on educational trends.

CIP codes are six-digit numbers where instructional programs are classified at the most granular level and are classified according to the two-digit and four-digit prefixes of the code.

Basically, “CIP” is an acronym you likely never heard of that’s actually pretty important.

Originally developed and published in 1980, CIP has been revised five times. The most recent revision was in 2020, with the 2020 update adding nearly 70 new four-digit series and more than 300 new six-digit codes.

Here are the four two-digit CIP codes relevant to this “professional” vs. “graduate” degree discussion:

01 - Agriculture (Veterinary Medicine)

22 - Legal Professions (Law)

39 - Theology (Divinity/Ministry)

51 - Health Professions (Medicine, Dentistry, Pharmacy, etc.)

Here are some tangible ways CIP codes are used:

Federal financial aid eligibility: Determines loan limits and program eligibility

STEM designation: Certain CIP codes qualify international students for STEM OPT visa extensions

Veteran benefits: Eligibility determined by CIP code assignment

Federal reporting: Used in Integrated Postsecondary Education Data System (IPEDS)

Data comparison: Allows comparing programs across different institutions

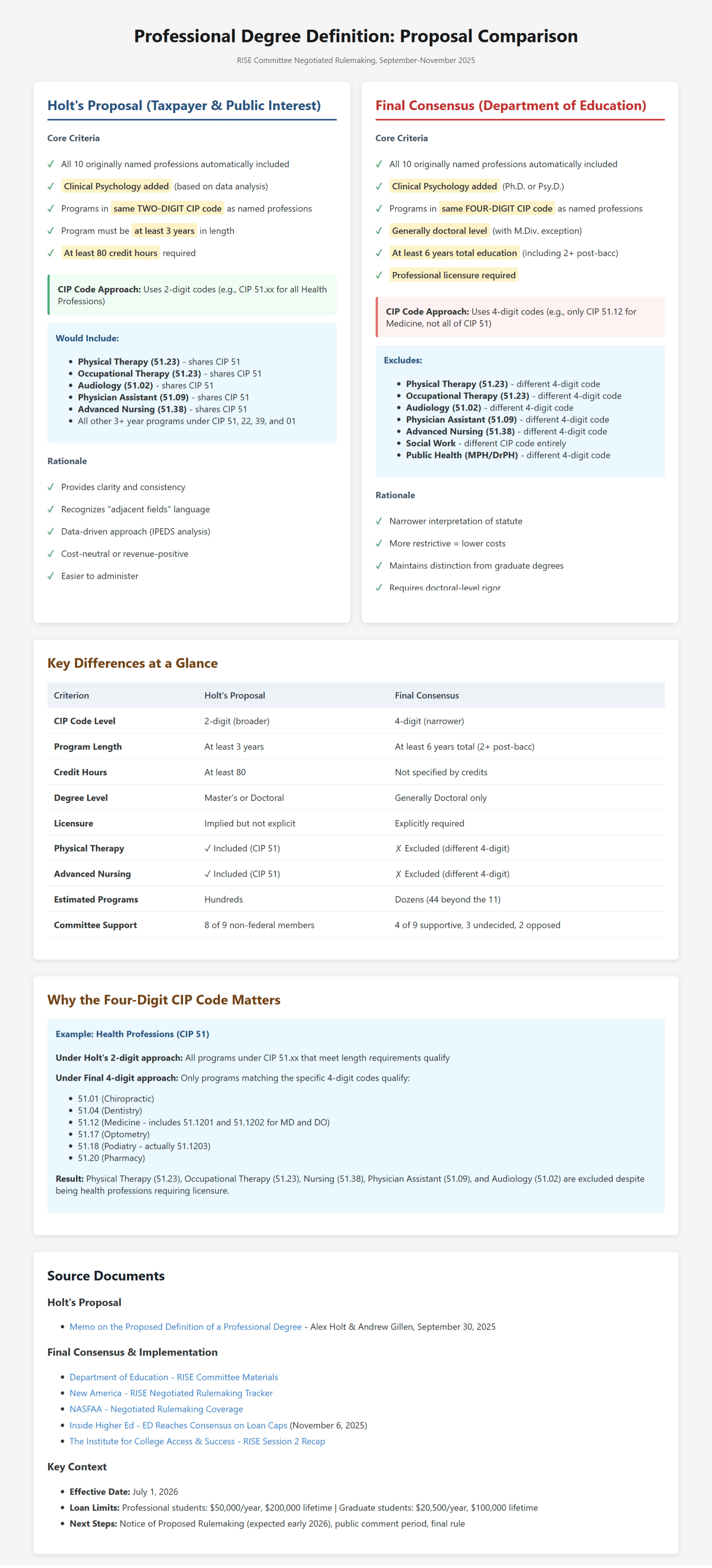

So in the process of the DOE trying to come to consensus around a proposed change, there was disagreement about how to decide what belongs in each bucket of professional vs. graduate degree. Alex Holt proposed a definition that would have included all the professions whose CIP codes started with the two digits 51.

His was not the proposal that advanced.

The pdf below is a copy of the memo where Alex Holt and Andrew Gillen submit their proposal. The first three pages are helpful to skim if you want to get even more granular.

|

So the difference between using 2-digit vs. 4-digit CIP codes is BIG in the context of the OBBBA and the DOE’s proposal.

2-digit approach: All programs under CIP 51 (Health Professions) would qualify if they meet other criteria

4-digit approach: Only programs with specific 4-digit codes like 51.12 (Medicine), 51.20 (Pharmacy) qualify

Here’s how it applies to my profession, for example: Physical Therapy (51.23) shares the same 2-digit code (51) with Medicine (51.12), but has a different 4-digit code from Medicine or any of the others specifically named as “professional” in the CFR, which is why it's excluded under the final consensus definition being proposed.

Here’s a fantastic comparison table between the more liberal, 2-digit definition proposed by Alex Holt and the final proposal. Claude created this with my prompting:

(click the link to read it more easily 👀)

That final proposal is expected to come out as a proposed rule and go through the Notice and Comment Rulemaking (NCRM) process.

What is this Really all About? Let’s Dive a Little Deeper. See What You Think! 🤿👇️

As noted, as a result of the passage of the 2025 tax and reconciliation bill (these types of bills are only passed when one party controls the Presidency and both Houses of Congress. I wrote about that here) signed by President Trump on July 4, 2025, the regulatory body who implements this part of the law must update the language on the Code of Federal Regulations.

This will reflect the new limits imposed by the bill for professional vs. graduate degree and the elimination of the Direct Plus program and its uncapped benefits. Since the definition of the degree type is now arguably even more important, they are taking the step to make that update through rulemaking.

If you want to read the section of the bill that lays this out, click the link to the bill here, then hit Control F on your keyboard and type this: 81001. This will take you to this section of the HR 1. It begins like this:

Here’s an example of a profession whose educational requirements for licensure have changed markedly over the last 25 years. My own profession, physical therapy, is now a program requiring a doctoral degree. It is a three year post-bachelor’s education program. For reference, when I graduated with my Master’s in 1998, the required degree to sit for the licensure exam was still only a Bachelor’s.

In 2002, the Master’s Degree was the minimum degree permitted for new graduates of accredited physical therapist programs sitting for the licensing exam. There was some variation in that degree. While I obtained a Master’s of Physical Therapy degree, others obtained a Master’s of Science in Physical Therapy degree.

In 2016, the Doctor of Physical Therapy degree became the minimum degree required to sit for the licensing exam. 1996 was actually the first year a school graduated a class of DPT students. That was Creighton University.

Transitional Doctor of Physical Therapy (tDPT) degrees were rolled out in the 1990s and became prolific in the coming years. The American Physical Therapy Association (APTA) set a 2020 goal for all practicing physical therapists to have the doctoral degree by 2020. I completed my tDPT with the University of Montana in 2020. For what it’s worth, I publicly and regularly call for all PTs with a lesser degree to complete their tDPT, practicing or not.

The Department of Education put out this statement on November 24th, 2025.

Here’s a quote:

President Trump’s One Big Beautiful Bill Act (the Act) placed commonsense limits on federal student loans for graduate degrees. These loan limits will help drive down the cost of graduate programs and reduce the debt students have to take out. Graduate students received more than half of all new federal student loans originated in recent years, and graduate student loans now make up half of the outstanding $1.7 trillion federal student loan portfolio.

Under the Act, the agency is required to identify “professional degree” programs that will be eligible for higher federal lending limits. A negotiating committee convened by the agency has proposed a consensus definition that designates Medicine (M.D.), Dentistry (D.D.S./D.M.D.), Law (L.L.B./J.D.), and several other high-cost programs as eligible for a $200,000 borrowing limit. Students who pursue a degree in other graduate or doctoral programs would be capped at $100,000 in federal loans. Undergraduate students are generally not affected by the new lending limits.

and this:

The Department of Education has not published a proposed or final rule defining professional student yet. Because the negotiated rulemaking committee unanimously agreed to a proposed definition for “professional student” for increased loan limits, among other things, the Department is required to publish the agreed upon language in its proposed rule. But the Department has not prejudged the rulemaking process and may make changes in response to public comments.

More of the Back Story on This Issue:

In May, the multi-year pause on the involuntary collection of defaulted student loans resumed. It had been paused since 2020. It seems like this change to limits in the One Big Beautiful Bill Act was likely at least partially to address the issue of defaulted federal student loans.

Recall that the OBBBA is a tax and reconciliation bill. By limiting how much people can borrow (and shrinking the exposure of taxpayers under the loan program), the government expects it will, on net, spend less over the next decade than previously projected. It goes into the “savings” column in the Congressional Budget Office’s calculation of the economic impact of the OBBBA.

Approximately 5.3 million ED-serviced borrowers with nearly $117 billion in outstanding federal student loans are in default as of June 2025, representing seven percent of the total $1.58 trillion portfolio.

And there's a "default cliff" looming: As of June 30, 2025, the ED-held loans of approximately 4.3 million recipients totaling about $103 billion are between 181 and 270 days delinquent. If these 4.3 million individuals with delinquent loans do not take action to cure their delinquency, they risk entering default in fall 2025, and the federal student loan portfolio may see an almost doubling of the number of defaulted loan recipients and of defaulted loan amounts.

34.4% of ED loan recipients, or more than six million recipients, are more than 30 days delinquent on their accounts. This includes more than four million recipients in late-stage delinquency who are at risk of defaulting in the next six months.

References and Additional Reading:

My take:

The federal government has the right to pass laws about the loans that they grant, including to place caps on loans. The issue is that the nomenclature and the categorization of professional vs. graduate degrees feels either arbitrary or directed at professions more commonly pursued by women. These caps may also exacerbate shortages in high-need professions like nursing. Those are some of the things I am hearing.

Here’s what could be a cleaner, more financial-planning focused solution: place caps that reflect the expected average salary year one of working in that profession while acknowledging that ALL are professions. This may also encourage more competition between schools offering the same professional degrees.

Okay, let me come clean. I didn’t make up the concept of “don’t take out more student loans than you will earn in your first year out of school.” I heard it on The Money Guy Show. They have repeated it several times and it sure stuck with me.

Here’s the co-host explaining the concept. Oh, and he means your total in school loans shouldn’t exceed what you will make year one, not just your graduate degree (professional education) school loans:

Let’s apply that to various health professions. Keep in mind that healthcare professions are only ONE of the categories of degrees covered in the CFR related to federal student loans:

Nursing: An Associate’s Degree is required and an RN might earn about $70,000 year one. If the nurse has a BSN instead of an ADN, they might start around $80,000. Nursing is an undergraduate degree with access to the subsidized loans.

Nurse Practitioner: a Master’s is required and year one, they earn about $125,000 per year. The total cap at $100,000 may not make sense. The annual cap may be too low.

Physical Therapist: A Doctoral Degree is required and year one, they might earn about $80,000. The total cap at $100,000 might make sense. The annual cap may be too low.

Doctor of Medicine or Doctor of Osteopathy: A Doctoral Degree is required and year one (after residency, when their salaries are lower), they might earn $200,000-$400,000+. Does the $200,000 cap make sense? Probably too low. The annual cap? Also probably too low.

All four of those examples are inarguably professions, to be absolutely clear!

Do the caps imposed all make sense based on the Money Guy Show’s recommendations?

Probably not.

Do the caps imposed make sense based on an arbitrary designation?

Probably not.

So how should caps on federal student loans be determined? Is this the “right” way?

Probably not.

And finally, for my PT friends, does the financial ROI of a PT degree make sense?

I’d have a really hard time making the argument that it does.

Federal Student Loans are Not the Only Loans, But They are Arguably the Best Loans

Graduate and professional students often turn to private, state-based, or institutional loans when federal limits are reached. Remember, subsidized loans are not available for graduate and professional degree programs.

Loan Type | Interest Rates | Repayment Flexibility | Protections (Deferment, Forgiveness) | Eligibility |

|---|---|---|---|---|

Federal Direct Unsubsidized | Fixed, around 8% (2025) | Very flexible | Strong borrower protections (IDR, PSLF, deferment) | All graduate/professional students |

Federal Grad PLUS (phasing out) | Fixed, around 9% | Flexible | PSLF eligibility, deferment options | Credit check required |

Private Loans | Variable 3–15% | Limited | Few protections, no forgiveness | Credit-based, cosigner often needed |

State-Based Loans | Fixed, often lower | Moderate | Varies by state program | Varies Significantly |

Institutional Loans | Varies by school | Limited | School-specific policies | Enrolled in specific programs |

Personal Loans/HELOCs | Variable, often high | Limited | No education-specific protections | Credit/collateral required |

President Donald J. Trump and his administration believe we can, and must, be better. Instead of maintaining the status quo that is failing American students, the Trump Administration’s bold plan will return education where it belongs — with individual states, which are best positioned to administer effective programs and services that benefit their own unique populations and needs.

State Loans Available Vary Significantly Based on the Particular State

Here’s a chart comparing Rhode Island’s program to Minnesota’s program (thank you to Copilot, who created this table and I lightly edited it):

Feature | Rhode Island Student Loan Authority (RISLA) | Minnesota SELF Loan Program |

|---|---|---|

Type of Program | Quasi‑state nonprofit loan authority | State‑run loan program via MN Office of Higher Education |

Eligibility | Available nationwide; any accredited U.S. school | Restricted to MN residents or students at MN schools |

Loan Amounts | $1,500 minimum; up to $50,000 annually; aggregate cap ~$200,000 | Covers gaps after grants/federal aid; no strict annual cap, limited by cost of attendance |

Interest Rates | Fixed APR ~2.99%–8.74% depending on term (5–15 years) | Fixed ~5.95%–6.45%; variable ~6.00%–6.50% (10–20 year terms) |

Repayment While in School | Full deferment available; no required in‑school payments | Requires $15 monthly payments while in school (may not cover accruing interest) |

Repayment Flexibility | Income‑based repayment option; deferment and forbearance available | Limited flexibility; deferment available but no income‑based repayment |

Borrower Protections | Forgiveness for death/disability; cosigner release; hardship forbearance | Deferment and transition periods; no forgiveness or cosigner release |

Unique Benefits | Internship reward ($2,000 forgiveness); Nursing reward (0% interest for 4 years for new RI nurses); autopay discount | Success Coaching program (goal setting, financial guidance); state oversight credibility |

Cosigner Requirements | Often required, but cosigner release possible | Cosigner required; no release option |

Target Audience | Broad — undergrad, grad, professional students nationwide | Narrow — MN residents or MN school attendees |

Honestly, I’m the most concerned about the limits on nurse practitioners and physicians, even with physicians in the higher cap bucket. Why? We desperately need more primary care medical providers. As I noted in my examples, NPs can reasonably earn around 130k early in their career, and primary care physicians can reasonably earn north of 200k early in their career. They should be able to take on and successfully repay a higher level of school loans than the new caps allow. These new caps are just unfortunate barriers. We need to grow this workforce, not make it harder to educate them.

For other professions, it’s hard to say what the impact will be. Here are a few of the possible sequalae I’ve been thinking about in general:

Some students will be dissuaded from accepting offers of admission. Students who accept admission will be the ones who can pay out of pocket or whose families can pay out of pocket, and who can patch together loans from the various sources available.

Universities will lower their prices. I’m skeptical of this one. Especially for NP programs and MD and DO programs, there aren’t enough programs to admit qualified candidates on top of the being a shortage of these providers to meet the needs of primary care. There aren’t enough qualified professors to even teach at the universities that offer them. That’s a story for another day.

Even fewer physicians will choose one of the primary care specialties. The size of medical school loans is so high already that many physicians say primary care isn’t even an option if they can get “matched” into a specialty residency. If they need to take out higher cost, higher-risk loans? Even less likely to opt into a primary care specialty! We NEED MORE internists, pediatricians, geriatricians, etc. In some underserved and rural areas, the barrier is already too great. They are in dire straits.

States will need to absorb some of the burden of student loan debt to support their residents and their state’s universities. Default rates risking add to the states’ possible risks.

A final word:

Parents and their young adult children entering post-secondary education should weigh the financial impacts of their educational decisions. Calculate the return on investment likely for both an undergraduate and graduate degree. Try to limit debt in undergraduate education and consider the Money Guy Show’s advice not to borrow more than you will likely earn your first year of working.

On the crisis of an undersupply of healthcare professionals and the exponential rise of education costs: We must graduate and retain individuals in healthcare professions who can succeed in their chosen profession, starting with being able to pay for their education and pay back their student loans. This change is unlikely to address this problem.

And when it comes to my own profession: It requires a doctoral degree and we have direct access status to the patient population. Yet our salary is similar to that of someone with an associate’s or bachelor’s degree in nursing and significantly lower than a less-educated MSN required for an NP degree and license. This is truly unsustainable. Reimbursement for therapists has to be higher to match the level of education and its cost to make the degree worth the time and money. Graduating highly educated professionals should mean they earn a higher average salary than other professions with lesser degrees. Shouldn’t that just be table stakes? I say it’s a sign of how undervalued the profession is to the stakeholders establishing the financial value of our services. Could professions become extinct?

We have many crises in healthcare in this country. To me, this latest headline issue is a chance to highlight one we don’t talk about enough when we talk about quality, access, and patient-centered care. That’s the cost and burden of educating our healthcare professionals.

It’s all connected.

*Disclaimer: All opinions and ideas expressed in this article are solely mine and none represent a recommendation or should be viewed as advisement of any kind to anyone to do anything.*

Reply